DISCLAIMER: the information contained in this tax tip are general comments only and do not constitute or convey advice perse. Individuals should seek their own independent advice from a qualified advisor to ascertain how the taxation law applies in their individual circumstance. The information contained is given in good faith and is believed to be accurate. However, neither Childcare Accounting & Financial Services nor any of its employees give any warranty of reliability or accuracy nor accept any responsibility in any way including by reason of negligence for errors or omissions herein.

Food & Drink

You are entitled to claim a deduction for food, drink and other refreshments provided to children as part of your day care activities. In order to claim these expenses you need to keep good records of the food purchases you make, particularly if you are registered for GST.

The easiest way to keep track of and calculate your food deduction(s) is to shop for day care items separately from the regular shop you do for yourself and your family. If this is not possible, then you must ensure that you can identify the items purchased for day care and those items which are private. You can do this by highlighting or marking those day care items on the shopping docket/receipt. Doing this as soon as possible after completing your shopping will ensure that you won't forget what you have purchased for day care.

If you are registered for GST it is important to note that some fresh foods and other items are GST free. You must therefore ensure that you are claiming the correct amount of GST.

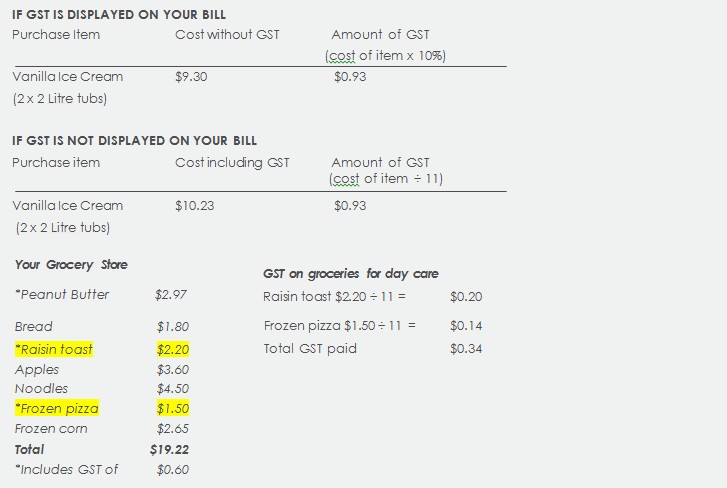

The amount of GST paid on your food bills is noted separately as a total amount on most supermarket dockets, with the foods that attract GST being marked with an asterisk (*). This makes the task of recording your food expenses, for both GST and income tax purposes, relatively easy. However, in some circumstances you may still be required to calculate the GST paid on your food and drink costs. you can do this by dividing the items that have attracted GST by 11, as per the following example.

The easiest way to keep track of and calculate your food deduction(s) is to shop for day care items separately from the regular shop you do for yourself and your family. If this is not possible, then you must ensure that you can identify the items purchased for day care and those items which are private. You can do this by highlighting or marking those day care items on the shopping docket/receipt. Doing this as soon as possible after completing your shopping will ensure that you won't forget what you have purchased for day care.

If you are registered for GST it is important to note that some fresh foods and other items are GST free. You must therefore ensure that you are claiming the correct amount of GST.

The amount of GST paid on your food bills is noted separately as a total amount on most supermarket dockets, with the foods that attract GST being marked with an asterisk (*). This makes the task of recording your food expenses, for both GST and income tax purposes, relatively easy. However, in some circumstances you may still be required to calculate the GST paid on your food and drink costs. you can do this by dividing the items that have attracted GST by 11, as per the following example.